Roof damage can be a huge headache for any homeowner. Whether it’s from a storm, fallen trees, or just wear and tear over time, the costs of repairs can really add up. But here’s the good news: if you have homeowner’s insurance, you may be able to get some financial relief by filing a claim. That said, navigating the insurance claims process can be tricky—especially with stricter policies and rising premiums.

So, if you ever find yourself dealing with roof damage, here’s a simple guide on how to file an insurance claim and avoid common mistakes that could cost you time and money.

Step 1: Assess the Damage and Act Quickly

The first thing you need to do after you notice roof damage is to act fast. The longer you wait, the worse the damage could get—and the harder it might be to get a fair payout from your insurance company. Trust me, I’ve been there, and waiting only makes everything worse.

Ensure Safety First: If the damage is severe, don’t risk climbing up to inspect the roof yourself. It’s best to check from the ground or take a look in your attic to see if there’s any water damage.

Take Photos and Videos: Documenting the damage is super important. Make sure to capture clear, detailed pictures and videos from multiple angles. Don’t skimp here—insurance companies often rely heavily on photos for claims. After my own claim.

Check for Leaks: If water is coming into your home, it’s crucial to stop it from spreading. A tarp over the damaged area can help protect your interior while you wait for the insurance process to kick in.

Review Your Policy: Take a few minutes to review your insurance policy. This might seem boring, but it’s important to understand what’s covered and what’s not. For example, some policies exclude things like wear and tear or lack of maintenance

Step 2: Contact Your Insurance Company

Once you’ve assessed the damage and taken photos, it’s time to contact your insurance company. Don’t wait too long—it’s always better to file sooner rather than later. The sooner they can get their adjuster out there, the quicker the process will move.

What to Expect When Filing a Claim

Provide the Details: You’ll need to give your insurance company all the basic details about the damage. This includes when it happened, what caused it (e.g., a storm or a fallen tree), and how extensive the damage is.

Get a Claim Number: Once your claim is filed, the insurance company will assign you a claim number. This will help track your case as it moves forward. Keep that number handy because you’ll need it anytime you call for updates or information.

Temporary Repairs Might Be Needed: Some policies require you to make temporary repairs to prevent further damage. This might include things like putting a tarp on your roof or sealing up leaks. Don’t forget to keep receipts for any temporary repairs, as they might be reimbursed.

Step 3: Get a Professional Roof Inspection

While your insurance company will send an adjuster to inspect the damage, it’s a good idea to hire a roofing contractor to do their own inspection.

Look for Insurance Experience: It’s best to hire a roofer who has experience working with insurance claims. They’ll know exactly what to look for and how to handle the process.

Get a Written Estimate: Your roofing contractor should provide you with a detailed, written estimate that outlines the extent of the damage, the cost of repairs, and the estimated time for completion.

Beware of “Storm Chasers”: After major storms, unlicensed contractors sometimes flood the area, offering quick fixes at low prices. Be cautious—these storm chasers can cause more harm than good. It’s better to go with a trusted, licensed roofer who will follow all the necessary codes and regulations.

Step 4: Work with the Insurance Adjuster

Now, the fun part: dealing with the insurance adjuster. While the adjuster’s job is to assess the damage and decide how much the insurance company will pay, they work for the insurer—not you. This means they may try to offer you less than you deserve.

How to Ensure a Fair Assessment

Be Present for the Inspection: If you can, be there when the insurance adjuster comes to assess the damage. It’s a good idea to have your roofing contractor with you too. They can point out things the adjuster might miss.

Compare Estimates: If the adjuster’s estimate is lower than your contractor’s, don’t be afraid to push back. You have the right to negotiate.

Request a Reinspection: If your claim gets denied or you feel the payout is too low, you can request a second inspection. It’s not uncommon for adjusters to miss some damage, and a second look can make all the difference.

Common Challenges Homeowners Face When Filing Roof Damage Claims

Filing a roof damage claim isn’t always straightforward. Here are some common challenges we’ve seen—and experienced myself:

Increased Claim Denials

Many homeowners face denied claims, especially as insurance companies tighten their policies. This is often because of the rising costs of storms and natural disasters. If your claim gets denied, don’t panic. Just make sure you have a detailed contractor report, lots of photos, and a good explanation to back up your claim.

Higher Deductibles

Some insurance policies now have higher deductibles for roof damage caused by storms, wind, or hail. These deductibles are often 2% to 5% of the value of your home, which can add up quickly. Check your policy before you file so you’re prepared for these costs.

Delays in Payouts

If you’re in an area hit by a major storm, be prepared for delays. Insurance companies often get overwhelmed with claims and can take longer to process them. Keep track of your communication with your insurer, and don’t hesitate to follow up if things seem to be moving too slowly.

Overcoming Insurance Claim Challenges

Know Your Policy: Always review your policy before you file a claim. Make sure you understand your deductible and what’s covered.

Document Everything: Take photos and videos of the damage and keep notes of all communications with your insurance company.

Negotiate: If you feel your settlement offer is too low, don’t be afraid to negotiate. Use estimates from your roofer to back up your case.

Consider a Public Adjuster: If your claim is denied or you’re getting a low settlement, a public adjuster can help you fight for a better payout.

Final Thoughts: Be Prepared Before You Need to File a Claim

Filing an insurance claim for roof damage doesn’t have to be a nightmare if you’re prepared. Keep these tips in mind:

Review your policy every year.

Schedule regular roof inspections to catch small issues before they turn into big ones.

Work with a trusted contractor who can help you through the claims process.

If you’re dealing with roof damage, don’t hesitate to reach out for help. At San Carlos Roofing, we’re here to provide expert inspections and guide you through the claims process. Contact us today!

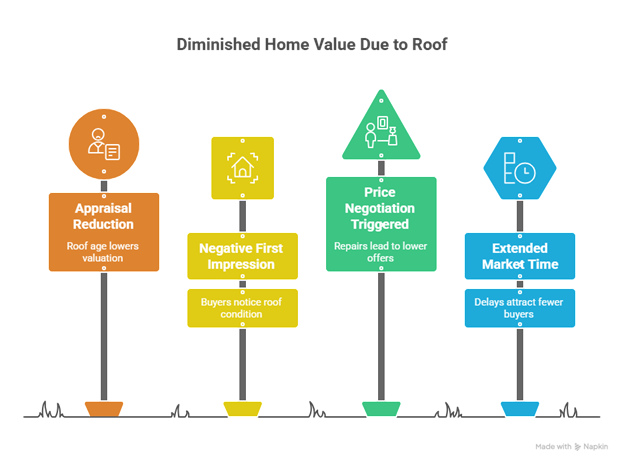

A home’s roof might not be the first thing buyers fall in love with, but it’s one of the first details they scrutinize. An aging, stained, or curling roof can instantly signal costly repairs ahead, putting your asking price in jeopardy. Industry research shows that a worn roof can reduce a home’s market value by $5,000 to $15,000 on average, and in some cases even more if serious structural issues are found during inspection.

Why Roof Condition Directly Impacts Appraisal

Appraisers factor roof age and condition into their valuations because it’s a major structural component. If the shingles are past their life expectancy or if leaks are present, appraisers often lower the estimated market value to account for anticipated replacement costs. That reduction ripples through the sale process, making it harder for buyers to secure financing at your desired price.

The Buyer’s First Impression

A roof covers every inch of the house, so its condition is impossible to hide. Missing shingles, faded color, or sagging lines catch the eye before buyers even step inside. First impressions matter: a roof that looks like it’s on its last legs immediately shrinks the buyer pool. People expect a turnkey purchase and rarely want to negotiate repairs right after moving in.

How Old Roofs Trigger Negotiations and Price Cuts

Buyers know a replacement can cost tens of thousands of dollars. During inspections, even small issues, soft spots, worn flashing, or water stains, can lead to requests for steep credits or a lower sale price. In competitive markets, those negotiations often end with sellers conceding far more than the cost of a proactive replacement would have been.

Longer Days on Market

Homes with obvious roof wear routinely spend extra weeks, or months, unsold. Each additional day on the market risks lower offers and greater carrying costs. Real estate agents consistently report that houses with visibly aged roofs take longer to attract serious buyers, especially in regions where storms and heavy rainfall increase risk.

Insurance Challenges and Higher Premiums

Insurance companies see older roofs as liabilities. Policies for homes with roofs over 20 years old often come with higher premiums or exclusions for wind and water damage. This raises ownership costs for buyers and can be a deal breaker during underwriting. A fresh roof replacement helps maintain affordable coverage and reassures both insurers and buyers.

Regional Concerns in Southwest Florida

In hurricane-prone areas like Southwest Florida, roof integrity is critical. Severe weather can expose hidden weaknesses in an older roof, making buyers especially cautious. A roof nearing the end of its life can scare away potential offers altogether. That’s why many sellers in coastal markets choose to work with trusted local pros like San Carlos Roofing to inspect and replace aging roofs before listing.

The Domino Effect on Resale Value

A compromised roof can lead to other problems, water intrusion, mold growth, and damaged insulation, that further erode home value. These secondary issues can balloon repair costs, triggering additional price reductions and inspection delays.

Why Proactive Replacement Pays Off

Installing a new roof before listing isn’t just a cosmetic update; it’s a value-preserving strategy. Studies show homeowners typically recover 60%–70% of the installation cost in resale price, while avoiding stressful negotiations and failed inspections. Partnering with an experienced contractor such as San Carlos Roofing’s new construction team ensures the work meets regional building codes and passes buyer scrutiny.

Hard Numbers: How Much Value You Lose

Industry data reveals that a roof past its prime can drag down resale price by $5,000 to $15,000, sometimes more in high-end neighborhoods. Buyers factor the cost of immediate replacement into their offers, and appraisers often follow suit. If a replacement is expected to cost $12,000, it’s common to see a purchase offer trimmed by that amount plus a little extra to cover inconvenience.

Buyer Psychology and Future Expenses

A worn roof screams “hidden costs.” Even if leaks aren’t visible, curled shingles or worn flashing tell buyers a major expense is around the corner. This perception reduces the number of interested parties and creates a mindset where every other house flaw feels more serious. In real estate, that hesitancy almost always translates to lower bids.

How Old Roofs Complicate Inspections

Home inspectors flag roof issues immediately. From brittle shingles to soft decking, even minor problems get noted. A detailed inspection report can spook cautious buyers or force sellers to accept hefty repair credits. According to leading real estate sources, inspection findings tied to an old roof are among the most common reasons for delayed or failed closings.

Appraisal Adjustments and Lending Hurdles

Appraisers know that replacing a roof isn’t optional. If they determine the roof has less than five years of life, they typically reduce the property’s value accordingly. Some lenders even require a roof certification or replacement before approving financing. This can derail a deal just days before closing, creating stress for everyone involved.

Insurance Costs That Scare Buyers

Older roofs increase the risk of leaks and storm damage, which insurance carriers translate into higher premiums. In hurricane-prone states like Florida, insurers may refuse wind coverage for roofs older than 15 to 20 years. Buyers factoring in steep premiums may lower their offers, or walk away. Installing a new roof replacement keeps premiums manageable and protects resale value.

Regional Pressures in Southwest Florida

In coastal climates, salt air, high humidity, and intense sun accelerate roof deterioration. Buyers in these markets are particularly cautious. They understand that an outdated roof might not meet modern building codes designed to withstand hurricanes. Local experts like San Carlos Roofing know the specific materials and installation methods that stand up to these harsh conditions, helping sellers avoid last-minute surprises.

Extended Time on Market and Price Reductions

An old roof can add weeks or months to a listing’s life. The longer a property sits, the more leverage buyers gain to negotiate a lower price. Sellers often end up reducing the asking price multiple times to attract offers, eroding profits well beyond the cost of a proactive replacement.

Energy Efficiency Losses Add Up

Aging roofs often have inadequate insulation or ventilation. Hot air leaks out in winter and seeps in during summer, leading to higher utility bills. Savvy buyers notice these inefficiencies, and many prefer homes with updated, energy-efficient roofing systems recognized by programs like Energy Star. Highlighting poor energy performance can further depress offers.

The Compounding Effect of Deferred Maintenance

An old roof rarely deteriorates in isolation. Moisture intrusion damages rafters, drywall, and even foundation elements over time. These hidden issues multiply repair costs and create a paper trail of maintenance problems that can discourage potential buyers and appraisers alike.

Steps to Protect Your Home’s Value

If your roof is approaching 20 years or shows visible wear, schedule a professional inspection before you list your home. A thorough evaluation pinpoints hidden leaks, sagging areas, and compromised flashing, allowing you to address problems early. Fixing small issues now can prevent a major price drop later.

Plan a Timely Replacement

Replacing the roof before selling might feel like a big expense, but it’s often the smartest financial move. Homeowners typically recoup 60%–70% of the cost in higher resale value while attracting more serious buyers. A well-timed upgrade, done a year or two before putting the house on the market, ensures warranties are transferable and the roof looks fresh during showings.

Market the Upgrade in Your Listing

Highlight a new roof in all marketing materials. Use clear language in the description, “Roof replaced in 2025 with 30-year architectural shingles”, and include photos that showcase its clean lines and modern materials. Mentioning the upgrade during open houses or on real estate platforms builds buyer confidence and sets your property apart.

Document the Work

Provide receipts, contractor details, and warranty information to potential buyers and their agents. Organized documentation not only builds trust but also helps the appraiser verify the value of the upgrade. This can speed up the closing process and protect you from last-minute price cuts.

Choose a Contractor With Local Expertise

Hiring a reputable local roofer is critical for both workmanship and compliance with regional codes. Trusted companies like San Carlos Roofing understand hurricane-resistant installation methods and the specific requirements of Southwest Florida’s climate. Their new construction services and roof replacement options ensure your investment is protected and market-ready.

Insurance and Financing Advantages

A new roof can qualify the property for lower home insurance premiums and simplify mortgage approvals for buyers. These financial perks become strong selling points, helping justify your asking price and giving your listing an advantage in a competitive market.

Boosting Curb Appeal for Faster Sales

A fresh roof transforms the home’s exterior and creates a polished look that photographs beautifully for online listings. Pair the upgrade with clean gutters, a painted front door, and well-kept landscaping to create a striking first impression that encourages strong offers.

Final Takeaway

An aging roof drags down home value, scares off buyers, and complicates appraisals and insurance. Proactive replacement, on the other hand, protects equity, enhances curb appeal, and supports a higher resale price. Treat the roof as a core investment rather than a last-minute repair, it’s one of the most powerful ways to preserve and grow your property’s market value.

Your roof isn’t just shingles and nails, it’s the first line of defense against Florida’s blazing sun, pounding rain, and sudden gusts. Over the years, heat, humidity, and storms gradually wear down materials. By the time a roof hits the 15–20 year mark, its ability to keep out moisture and regulate indoor temperatures starts to weaken. Cracked shingles, curling edges, and worn flashing might look like minor problems, but they are warning signs that the entire system is ready to fail.

Small Leaks, Big Bills

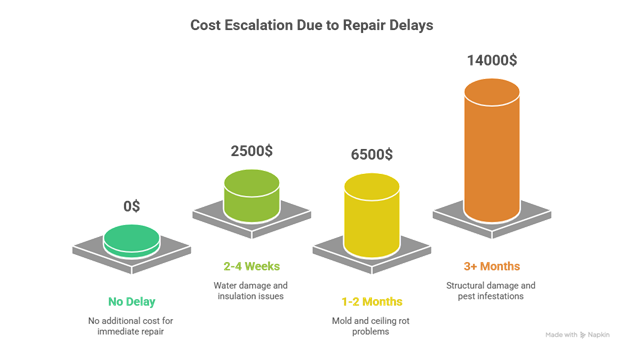

A single overlooked leak can quickly spiral into thousands of dollars in repairs. Recent industry data shows that waiting just two weeks to patch a leak can add roughly $1,500 in water damage costs. Stretch that delay to two months, and you could be staring at an extra $8,000 in structural repairs and mold remediation. Water that slips past aging shingles seeps into insulation, drywall, and wooden supports, where it rots and warps everything in its path.

The difference between acting now and waiting even a month is the difference between a modest repair bill and a full-blown disaster that forces you to replace walls, ceilings, and electrical wiring.

Insurance Gaps That Surprise Homeowners

Many homeowners assume their insurance will swoop in if a storm rips off shingles or a leak floods the attic. The truth is more complicated. Most policies contain clauses that deny coverage if a roof is past its life expectancy or if the insurer deems damage to be caused by neglect. That means a roof that’s 20 years old, or even 15 years old in hurricane-prone regions, can leave you footing the entire bill.

Insurers increasingly inspect homes before renewing policies, and a worn or sagging roof can be a deal-breaker. If the inspector flags it, you may be forced to replace the roof before coverage continues. In some cases, a neglected roof can even void a claim after a storm, shifting all costs back onto the homeowner.

Escalating Energy Costs

An aging roof does more than leak water; it leaks energy. As shingles crack and insulation deteriorates, your home’s building envelope loses its efficiency. Air conditioning systems must work harder to maintain a comfortable temperature, driving up monthly energy bills. Homeowners who delay roof replacement often notice subtle spikes in electric costs, another quiet drain on your wallet that adds up over time.

If you plan to sell your home, an old roof can send buyers running or at least negotiating for a hefty discount. According to the National Association of Realtors Remodeling Impact Report, a new roof can add up to $12,000 to resale value. Buyers know that an old roof means immediate replacement costs, and they will factor that into their offers or walk away entirely.

A fresh roof, on the other hand, signals that the home is well maintained and ready for the next decade. It’s an investment that pays for itself when it’s time to put up the “For Sale” sign.

Real Numbers: The Cost Escalation Table

Delay Period

Immediate Repair

Damage from Waiting

New Cost Estimate

Additional Cost

No Delay

$500–$1,500

None

$500–$1,500

$0

2–4 Weeks

$500–$1,500

Water damage/insulation

$2,000–$5,000

$1,500–$3,500

1–2 Months

$500–$1,500

Mold/ceiling rot

$5,000–$10,000

$4,500–$8,500

3+ Months

$500–$1,500

Structural damage/pests

$10,000–$20,000+

$9,500–$18,500+

These figures aren’t scare tactics; they reflect real outcomes that roofing contractors see every season. Waiting transforms a manageable repair into a gut renovation.

Local Expertise Matters

For homeowners in Southwest Florida, professional guidance is crucial. A trusted contractor like San Carlos Roofing offers thorough inspections and honest assessments so you know exactly when it’s time to replace rather than patch. Their roof replacement services are tailored to Florida’s climate, using materials that stand up to relentless sun and sudden storms.

Roofing experts will evaluate shingles, underlayment, flashing, and attic ventilation, spotting weaknesses you might never see from the ground. Acting on their advice before disaster strikes can save you thousands and protect your home’s long-term value.

Safety Isn’t Optional

Beyond money, an aging roof is a safety hazard. Loose shingles can become dangerous projectiles during high winds. Water intrusion can compromise electrical wiring, increasing fire risks. Mold growth from chronic leaks can trigger allergies and respiratory issues for anyone living inside. What starts as a “minor” drip can create health problems that far outweigh the cost of a replacement.

Structural Dangers and Hidden Risks

Moisture: The Silent Destroyer

Water doesn’t just wet wood, it transforms it. When an old roof allows rain to seep into rafters and joists, the lumber swells and slowly loses strength. Over time, this can lead to sagging ceilings or even partial collapses. According to the National Institute of Building Sciences, chronic moisture exposure is one of the leading causes of structural failure in residential homes. A slow leak hidden behind drywall can take months to show visible signs, but by then the damage is extensive and costly to reverse.

Mold and Indoor Air Quality Issues

A damp attic is a breeding ground for mold and mildew. Spores travel through HVAC systems and spread through every room, triggering allergies, asthma, and respiratory infections. Cleaning an entire home’s ventilation system and eradicating mold colonies can easily exceed $5,000–$10,000. Worse, homeowners’ insurance often refuses to cover mold that results from neglect.

Certified inspections by groups such as the Environmental Protection Agency confirm that untreated leaks dramatically increase indoor air pollutants. What seems like a harmless brown stain on the ceiling could be a health hazard affecting every family member.

Pests Find the Weak Spots

Rodents, raccoons, and insects love the small openings that appear in worn shingles and flashing. Once inside, they can chew insulation, gnaw wiring, and leave behind droppings that contaminate living spaces. Exterminating pests and repairing chewed electrical systems can cost more than a straightforward roof replacement.

Florida homeowners are especially vulnerable because warm weather keeps pests active year-round. A single loose vent or cracked soffit can invite an infestation that spreads quickly and requires expensive structural remediation.

Outdated Roofs vs. Modern Building Codes

Roofing codes are not static. Over the last decade, states like Florida have tightened requirements to improve hurricane resistance and energy efficiency. An older roof often fails to meet current wind-resistance standards or underlayment specifications.

If your roof predates these code updates, you could face fines or be forced to replace the roof before selling the house. Municipal inspectors can halt a home sale or new insurance policy until upgrades are completed. By proactively replacing the roof with code-compliant materials, you avoid bureaucratic delays and potential penalties.

Insurance Repercussions and Fine Print

Insurance companies look closely at roof age when underwriting policies. Many providers deny claims if the roof is over 15 years old, even if the homeowner maintained it. If you delay replacement and a major storm hits, you may find yourself responsible for every penny of the repair.

Insurers also evaluate whether damage stems from owner neglect. A small leak ignored for months is a perfect reason to deny coverage. The bottom line: an old roof is a financial liability that puts your entire home at risk of uncovered losses.

Real-Life Example of Cost Escalation

Consider a homeowner in Fort Myers who postponed replacing a 20-year-old asphalt roof to “save money.” After a heavy summer storm, hidden leaks led to soaked insulation and rotted roof decking. By the time the damage was discovered, repair estimates soared past $18,000, including structural reinforcement and interior drywall replacement. A full roof replacement at the first sign of failure would have cost roughly half that amount and preserved the home’s market value.

Fire Hazards from Electrical Exposure

Water infiltration doesn’t just damage wood, it threatens your wiring. Moisture around junction boxes and outlets can cause short circuits, sparking electrical fires. The National Fire Protection Association has long warned that water-damaged electrical systems present one of the most overlooked fire risks in residential properties.

Aging roofs with loose flashing or degraded seals allow just enough water to trickle into these critical areas, creating a hazard that often goes unnoticed until it’s too late.

Long-Term Energy Loss

A roof past its prime is a constant energy drain. Damaged insulation allows conditioned air to escape while outdoor heat seeps in. Air conditioners run longer, raising utility bills and accelerating wear on HVAC equipment. Over several summers, these added costs can surpass the price of a new, energy-efficient roof.

A modern replacement with reflective shingles and proper ventilation, such as those offered by San Carlos Roofing’s new construction services, can cut cooling expenses significantly and reduce your home’s carbon footprint.

The Myth of “Just Another Patch”

Some homeowners believe another layer of shingles will buy time. In reality, adding layers can trap moisture, add weight, and accelerate structural decline. Multiple layers make it harder to identify leaks and can even void certain manufacturer warranties. Professional roofers consistently warn that repeated patch jobs are short-term fixes that lead to higher costs later.

Preparing for a Smart Replacement

Addressing these dangers means more than simply calling a contractor when shingles fall off. A proper roof replacement involves a full inspection of decking, flashing, ventilation, and insulation. Quality installers provide written estimates, detailed timelines, and warranty information. Choosing a reputable local company like San Carlos Roofing ensures materials and installation meet strict Florida building standards and manufacturer guidelines.

The Smart Money Is on Replacement

The ROI of a Timely Roof Replacement

Spending money on a new roof might feel like a big hit, but it’s an investment that pays back quickly. Studies from the National Association of Realtors show that homeowners recoup an average of 60–85 percent of the cost when selling. Add in the savings on energy bills, maintenance, and insurance premiums, and a well-planned replacement can actually cost less over ten years than endless repairs on a failing roof.

Curb Appeal and Market Value

A fresh, clean roof transforms a home’s exterior instantly. Buyers see a property that’s been cared for and protected, and they’re willing to pay for that peace of mind. Many real estate agents report offers coming in thousands higher for homes with new roofs compared to those needing immediate work. Even if you aren’t selling soon, your property’s appraisal value benefits the moment the last shingle is nailed down.

Lower Insurance Premiums

Insurance carriers reward proactive homeowners. Replacing a roof before it becomes a liability can lower premiums because the risk of water intrusion, fire, and wind damage drops significantly. Many companies offer discounts for impact-resistant or energy-efficient materials, which is another reason to act sooner rather than later.

Planning Your Project Without Surprises

A smart replacement starts with a detailed inspection and a clear estimate. Look for contractors who:

Provide a written scope of work and firm pricing

Show proof of licensing and liability insurance

Offer manufacturer-backed warranties

Working with an experienced team like San Carlos Roofing ensures you get accurate assessments and transparent pricing. Their crew understands Florida’s weather extremes and uses materials engineered to handle heavy rain, blistering sun, and hurricane-force winds.

Choosing the Right Materials

Not all roofs are created equal. Modern shingles and metal systems offer better wind ratings, reflective coatings for heat reduction, and longer warranties than products from even a decade ago. Your contractor can explain options, architectural shingles, standing-seam metal, or energy-efficient tile, and match them to your budget and style.

Scheduling for Best Results

Florida’s rainy season and hurricane windows make timing critical. Aim for spring or early winter when weather is more predictable and crews are less booked. This reduces the risk of weather delays and may even net you off-season pricing.

Financing Options to Ease the Upfront Cost

If the initial investment feels steep, financing programs can spread payments over time. Some lenders offer low-interest home improvement loans, and certain municipalities provide energy-efficiency incentives for reflective or solar-ready roofs. Pairing these options with the long-term energy savings creates a manageable payment plan that pays off.

Eco-Friendly Upgrades

Consider adding solar-ready decking or reflective “cool roof” materials during replacement. These upgrades lower cooling costs and may qualify for Energy Star rebates or local tax incentives. The environmental benefits, less heat absorbed, smaller carbon footprint, are a bonus that modern buyers appreciate.

Why Local Expertise Counts

Roofing in Florida isn’t like roofing in a mild climate. High humidity, salt air, and hurricane-force winds demand precise installation and durable materials. A locally rooted company like San Carlos Roofing’s roof replacement team understands regional codes and can recommend the best products for long-term protection.

Final Word: Don’t Wait Until It Leaks

An aging roof is a ticking financial clock. Delay means more than a bigger repair bill, it means higher energy costs, insurance headaches, potential health issues from mold, and lost resale value. Acting now protects both your wallet and your family’s safety.

Bottom Line Replacing a roof before it fails is one of the smartest investments a homeowner can make. From safeguarding your home’s structure to boosting resale value and slashing energy costs, the benefits far outweigh the upfront price. Secure your property, lock in insurance coverage, and enjoy the peace of mind that comes from knowing the sky above your family is protected.

When it’s time to replace your roof, understanding the installation process can help alleviate concerns and ensure you know what to expect. A roof replacement is a significant investment in your home, so being informed about the steps involved can help you make better decisions and prepare for the project. San Carlos Roofing offers a comprehensive look at the roof installation process:

1. Initial Inspection and Estimate

The first step in the roof installation process is a thorough inspection by a professional roofing contractor. They will assess the current condition of your roof, identify any underlying issues, and measure the roof to provide an accurate estimate. This estimate will include the cost of materials, labor, and any additional services required.

2. Choosing Materials

After the inspection, you’ll need to choose the roofing materials for your new roof. Common options include asphalt shingles, metal roofing, and tile. Each material has its own advantages, lifespan, and cost considerations. Your contractor can help you select the best option based on your budget, aesthetic preferences, and the climate in your area.

3. Preparing the Site

Before the actual installation begins, the site must be prepared. This involves protecting your property, such as covering landscaping and placing tarps to catch debris. Ensuring a clean and safe work environment is crucial for both the workers and your home.

4. Removing the Old Roof

The next step is the removal of the existing roof. The old shingles, underlayment, and any damaged decking are stripped away to expose the roof’s structure. This process can be noisy and create a significant amount of debris, which the contractor will handle and dispose of properly.

5. Inspecting and Repairing the Roof Deck

With the old roof removed, the roof deck is inspected for any signs of damage or rot. Any necessary repairs or replacements are made to ensure a solid foundation for the new roofing materials. This step is crucial for the longevity and performance of your new roof.

6. Installing the Underlayment

Once the roof deck is in good condition, the next step is installing the underlayment. The underlayment is a protective layer that helps to prevent moisture from penetrating the roof deck. It also provides an additional barrier against the elements and can improve the overall performance of the roofing system.

7. Installing Flashing

Flashing is installed around any roof penetrations, such as chimneys, vents, and skylights, to prevent water infiltration. Properly installed flashing is essential for protecting these vulnerable areas and ensuring the longevity of your roof.

8. Installing the New Roofing Material

With the underlayment and flashing in place, the new roofing material is installed. The installation method varies depending on the type of material chosen. For example, asphalt shingles are nailed in overlapping rows, while metal panels are secured with screws and fasteners. The contractor will follow the manufacturer’s guidelines to ensure a proper installation.

9. Final Inspection

After the new roof is installed, a final inspection is conducted to ensure everything is done correctly. The contractor will check for any issues, such as loose shingles or improper flashing, and make any necessary adjustments. This step ensures that the roof meets industry standards and will provide reliable protection for your home.

10. Cleanup and Disposal

Once the installation and inspection are complete, the contractor will clean up the site, removing any debris and leftover materials. Proper disposal of the old roofing material and waste is handled by the contractor, leaving your property clean and safe.

11. Post-Installation Care and Maintenance

After the installation, your contractor will provide information on caring for and maintaining your new roof. Regular inspections and maintenance can help extend the life of your roof and prevent potential problems. Your contractor may also offer a warranty for their work, providing peace of mind and protection for your investment.

Closing thoughts

Understanding this process can help you feel more confident and prepared when it’s time to replace your roof. By knowing what to expect at each stage, you can ensure a smooth and successful roofing project that enhances the safety, value, and appearance of your home. Always choose a reputable and experienced roofing contractor to guide you through the process and deliver quality results. Call San Carlos Roofing for a prompt response answering your roofing questions.

Choosing the right roofing material for your home depends on several factors, such as climate, budget, aesthetics, and durability. San Carlos Roofing offers a guide to help you decide:

1. What Kind Of Climate Are You In?

Different roofing materials perform better in certain climates:

Asphalt Shingles: Affordable and durable, they perform well in moderate climates.

Metal Roofing: Ideal for areas with heavy rainfall, snow, or high winds. It’s also energy-efficient in hot climates as it reflects heat.

Clay or Concrete Tiles: Great for hot, sunny climates, offering excellent heat resistance.

Slate: Perfect for areas with freezing temperatures as it’s highly resistant to harsh weather.

Wood Shingles/Shakes: Suitable for dry climates but not recommended for regions with heavy rain or fire hazards.

2. WhatAesthetics and Architectural Styles Are You Considering?

Your roof should complement the style of your home:

Asphalt Shingles: Available in a variety of colors and styles, fitting most traditional homes.

Clay/Concrete Tiles: Best suited for Mediterranean, Spanish, or Southwestern-style homes.

Slate: Adds a timeless, elegant look, suitable for historic or luxury homes.

Metal Roofing: Modern and sleek, often seen on contemporary or rural homes.

Wood Shakes: Offers a rustic, natural appearance for cottages or cabins.

3. AreDurability and Lifespan An Issue?

Asphalt Shingles: Typically last 20-30 years.

Metal Roofing: Can last 40-70 years with proper care.

Clay/Concrete Tiles: Extremely durable, lasting over 50 years.

Slate: One of the most durable options, with a lifespan of up to 100 years.

Wood Shakes: Last 20-40 years, but require regular maintenance.

4. IsEnergy Efficiency Important?

Metal Roofing: Reflects heat and helps reduce energy costs in warm climates.

Clay/Concrete Tiles: Naturally insulating, reducing energy consumption.

Asphalt Shingles: Less energy-efficient but can be paired with reflective coatings.

5. Realistically, What’s YourBudget?

Costs vary depending on the material:

Asphalt Shingles: Most affordable option.

Metal Roofing: More expensive upfront but offers long-term savings in energy and maintenance.

Clay/Concrete Tiles: Moderately expensive but long-lasting.

Slate: One of the most expensive materials but highly durable.

Wood Shakes: Price can vary but typically falls between asphalt and metal roofing.

6. DoMaintenance Requirements Matter?

Asphalt Shingles: Minimal maintenance.

Metal Roofing: Low maintenance, but occasional inspections are recommended.

Clay/Concrete Tiles: Very low maintenance but may require occasional tile replacement.

Slate: Requires professional maintenance due to its weight and specialized installation.

Wood Shakes: Requires regular cleaning and treatment to prevent mold, rot, or pests.

7. Are You Familiar With Local Building Codes?

Check with your local building authority for regulations or restrictions on certain roofing materials. Some materials may require additional structural support, like slate or clay tiles, due to their weight.

8. Environmental Impact Matters. Is It A Priority For You?

If sustainability is a concern:

Metal Roofing: Often made from recycled materials and is fully recyclable.

Slate and Clay/Concrete Tiles: Natural materials with low environmental impact.

Asphalt Shingles: Typically, less eco-friendly, though some options use recycled content.

Evaluate your home’s architectural style, climate, and budget when choosing roofing materials. Durability, maintenance, and energy efficiency are key factors to consider, and consulting a roofing professional can help ensure you make the best choice for your home. San Carlos Roofing has over 30 years of local experience helping home and business owners alike make the right decision when it comes time to select the right roofing material for the job.

Roof repairs and replacements are significant investments, making them a prime target for scammers. Unfortunately, roofing scams can leave homeowners with shoddy workmanship, incomplete projects, or financial losses. To protect yourself from these fraudulent tactics, it’s important to know the common roofing scams and how to avoid them. San Carlos Roofing offers what to watch out for and how to ensure you’re dealing with a legitimate roofing contractor.

The “Storm Chaser” Scam

Storm chasers are unscrupulous contractors who show up after a major storm, offering quick repairs to homeowners who may have sustained damage. They often go door-to-door, claiming they’ve noticed damage to your roof and can fix it at a reduced rate or through your insurance.

Red Flags:

– The contractor pressures you to sign a contract immediately.

– They offer a “limited-time” discount or say they are “working in the area.”

– They claim to have leftover materials from another job and offer a discounted rate.

– The contractor wants to begin work before an insurance adjuster inspects the roof.

How to Avoid It:

– Never agree to work with a contractor who shows up unannounced. Take your time to research roofing companies and check their credentials.

– Call your insurance company and arrange for an adjuster to inspect your roof before committing to any repairs.

– Ask for references and review their past work to ensure they’re legitimate.

Upfront Payment Scam

In this scam, a roofer will ask for a large upfront payment before starting the job. Once they receive the money, they may disappear, or worse, they’ll complete the job with subpar materials and leave you to deal with any future issues.

Red Flags:

– The contractor asks for a substantial deposit or full payment before starting work.

– They offer an unusually low price that seems too good to be true.

– They are unwilling to provide a written contract or detailed estimate.

How to Avoid It:

– Always get a detailed contract that outlines payment schedules. Legitimate contractors typically require a small deposit upfront (no more than 10-30%), with the remaining balance paid after the job is completed to your satisfaction.

– Be cautious of any contractor who insists on full payment before any work begins.

– Use a credit card for deposits and payments, when possible, as this offers more protection than paying in cash.

Insurance Fraud Scam

Some contractors may suggest committing insurance fraud to get a new roof at little to no cost. They might advise inflating the cost of repairs or replacing a roof that doesn’t need replacement, then pocket the difference between the insurance payout and the actual cost of the work. Engaging in such a scam can result in serious legal consequences for both the contractor and the homeowner.

Red Flags:

– The contractor offers to waive your insurance deductible or says they can work the numbers to make the insurance company cover more than they should.

– They encourage you to file a claim for damage that doesn’t exist or is minor.

– They offer to handle your entire insurance claim without your involvement

How to Avoid It:

– Only work with contractors who follow ethical practices and operate transparently.

– Always be directly involved with your insurance company and adjuster throughout the claim process.

– Understand that attempting to commit insurance fraud is illegal and could result in fines or criminal charges.

The “Low-Ball” Estimate Scam

Some roofing scammers will offer a very low estimate to win your business, only to add on unexpected costs or cut corners during the job. This can result in poor-quality work, unfinished projects, or costly repairs down the road.

Red Flags:

– The initial quote is significantly lower than other estimates.

– The contractor isn’t clear about what is included in the price or avoids providing a detailed written estimate.

– They suggest vague, unverified problems with your roof that need urgent attention.

How to Avoid It:

– Get multiple quotes from reputable roofing contractors to compare prices.

– Be wary of estimates that seem too good to be true—quality materials and skilled labor come at a cost.

– Request a detailed breakdown of all costs in writing, and make sure the scope of work is clearly defined before the project begins.

Unlicensed or Uninsured Contractors

Some scammers pose as legitimate contractors but lack the proper licenses, insurance, or certifications to perform roofing work. If something goes wrong during the project or after, you may be left with no recourse for repairs or compensation

Red Flags:

– The contractor refuses to provide proof of licensing or insurance.

– They avoid signing a contract or providing written guarantees on their work.

– The contractor seems inexperienced or lacks a professional presence (e.g., no website, no reviews, no company vehicle or branding).

How to Avoid It:

– Always verify the contractor’s license and insurance. You can check with your local licensing board to ensure they are legitimate.

– Request proof of liability insurance and workers’ compensation coverage before any work begins.

– Make sure the contractor provides a written contract that includes guarantees or warranties for their work.

Inflated Damage Claims

In this scam, a roofer may exaggerate the extent of the damage to your roof in order to charge more for unnecessary repairs or replacements. They may even show you staged photos or fabricated evidence to justify the extra costs.

Red Flags:

– The contractor insists there is severe damage, but you haven’t noticed any visible issues.

– They refuse to explain the damage in detail or show you the specific problem areas.

– They suggest replacing the entire roof when minor repairs suffice.

How to Avoid It:

– Get a second opinion from another roofing contractor or an independent inspector before agreeing to major repairs.

– Ask the contractor to walk you through the specific areas of damage and explain why the work is necessary.

– Be cautious of contractors who pressure you to replace your roof prematurely.

“Free Roof” Scams

This scam targets homeowners by claiming they are eligible for a “free roof” due to supposed storm damage. The scammer will encourage you to file a fraudulent insurance claim, promising to handle everything on your behalf. In reality, this often leads to denied claims or shoddy work, leaving you responsible for the costs.

Red Flags:

– The contractor promises a “free” roof or implies that you can get a new roof without any out-of-pocket costs.

– They pressure you into signing an agreement that allows them to work directly with your insurance company without your involvement.

– They recommend filing a claim even when no damage is apparent.

How to Avoid It:

– Be cautious of any contractor who promises something for “free,” as this is rarely the case.

– Contact your insurance company directly to verify any claims or offers.

– Always inspect your roof for legitimate damage before agreeing to file an insurance claim.

Roofing scams can be costly and stressful, but by knowing the warning signs and taking precautions, you can protect yourself and your home. San Carlos Roofing suggests to always research contractors, verify their credentials, and avoid rushing into agreements without proper documentation. By staying informed, you can ensure your roofing project is completed by a trustworthy professional, saving you from potential headaches and financial losses down the road. Source : National Insurance Crime Bureau “Roofing fraud requires vigilance”

How San Carlos Roofing Protects Your Home from Weather Damage

When you’re searching for a roofing company in Southwest Florida, you’re probably asking yourself: “How do I know this company truly understands the unique challenges my roof faces? Will they actually protect my investment, or just patch things up temporarily?”

You’re right to be concerned. Southwest Florida’s extreme weather, intense sun, torrential rain, hurricanes, and more, puts your roof through conditions that roofers in other parts of the country never deal with. You need a company that doesn’t just know roofing, they need to know Southwest Florida roofing inside and out.

With 30 years of experience serving Fort Myers, Cape Coral, Naples, and surrounding communities, San Carlos Roofing has protected hundreds of Southwest Florida homes from our region’s toughest weather. We’re licensed (FL License #CCC1330248), insured, and proud to be recognized as a 2024 Nextdoor Neighborhood FAVES Winner by the homeowners we serve.

Here’s how we address the most common concerns homeowners have when choosing a roofing contractor:

“Will This Company Actually Understand Southwest Florida’s Weather Challenges?”

Your Concern: You’ve heard horror stories about roofing companies using materials or techniques that work fine up north but fail miserably in Florida’s climate. You need someone who genuinely understands what your roof is up against year after year.

How San Carlos Roofing Addresses This:

After three decades and hundreds of roofs in Southwest Florida, we know exactly what works, and what doesn’t, in our climate. We’ve seen it all: Hurricane Ian, Hurricane Irma, scorching summers, torrential rainstorms, and everything in between.

We know that:

Sun and UV damage is relentless here. We don’t just install any shingles, we recommend and install UV, resistant materials and reflective, lighter, colored options that actually reduce heat absorption and extend your roof’s life. After 30 years, we know which materials hold up to our intense sun and which fail prematurely.

Our heat is different. With proper attic ventilation systems, we prevent heat buildup that causes shingles to deteriorate faster, a critical detail many roofers overlook. Poor ventilation can cut your roof’s lifespan in half in Southwest Florida’s climate.

Hurricane, force winds aren’t hypothetical here. We reinforce roofs with hurricane straps, additional fasteners, and proper clips to secure shingles, because we’ve seen firsthand what cutting corners costs homeowners after major storms. Our installations meet and exceed Florida Building Code requirements specifically designed for high, wind zones.

“How Do I Know They’ll Catch Problems Before They Become Expensive Disasters?”

Your Concern: You don’t want to pay for a new roof in five years because small issues were missed or ignored. You need a company that’s proactive, not reactive.

How San Carlos Roofing Addresses This:

We offer no, obligation inspections because we believe in catching problems early, it’s saved our customers thousands of dollars over our 30 years in business. During our inspections, we:

Check for early signs of sun damage, warping, and brittleness before they lead to leaks

Inspect for water stains, damp spots, and damaged shingles that signal potential leaks

Assess your gutters and downspouts to ensure water flows properly (clogged gutters cause water backup and roof damage)

Look for loose or damaged shingles that wind could exploit during the next storm

Identify vulnerable areas after storms, especially hail damage that may not be obvious to homeowners

Our approach: Regular maintenance and inspections save you thousands in the long run. We document everything and give you honest assessments, no scare tactics, just facts backed by three decades of experience. Our customers appreciate that we tell them what they need to know, not what will generate the biggest invoice.

“Will They Use Quality Materials or Just Whatever’s Cheapest?”

Your Concern: You’ve heard that some contractors use inferior materials to boost their profit margins, leaving you with a roof that fails prematurely.

How San Carlos Roofing Addresses This:

After installing hundreds of roofs over 30 years, we recommend materials based on your specific needs and Southwest Florida’s demands, not our profit margin. We’ve learned which products truly perform in our climate and which marketing claims don’t hold up in real, world conditions.

We recommend:

Impact, resistant shingles for areas prone to hail and hurricane debris

Waterproof underlayment to prevent moisture penetration during our heavy summer rainfall

Metal or synthetic shingles that handle temperature fluctuations without cracking or warping

Zinc or copper strips to prevent moss and algae growth (a common Southwest Florida problem that can void warranties if left untreated)

We explain why we’re recommending each material and how it protects your specific home. Transparency is part of our service, and a big reason we’ve earned our reputation and our 2024 Nextdoor Neighborhood FAVES award.

“What About Hurricane Season? Will My Roof Actually Hold Up?”

Your Concern: You’ve seen neighbors lose shingles, or worse, during storms like Hurricane Ian and Hurricane Irma. You need confidence that your roof can handle Southwest Florida’s hurricane season.

How San Carlos Roofing Addresses This:

We’ve been through every major hurricane to hit Southwest Florida over the past 30 years. Hurricane preparedness isn’t an add, on for us, it’s built into every roof we install or repair:

We secure loose shingles and reinforce flashing (the seals at roof joints) to prevent wind from getting underneath

We trim or recommend trimming overhanging branches that could become dangerous projectiles

We reinforce roof structures with hurricane, rated fasteners and straps that meet Florida’s stringent High Velocity Hurricane Zone (HVHZ) standards

After storms, we provide prompt inspections to assess and document damage for insurance claims, we know exactly what insurance adjusters look for

Our commitment: We don’t just build roofs to code, we build them to survive Southwest Florida’s worst weather. Our track record of hundreds of successful installations speaks for itself, as do our customer reviews on Google and Angie’s List.

“Will They Actually Stand Behind Their Work?”

Your Concern: You’ve heard about roofing companies that disappear after installation or make it impossible to get callback service.

How San Carlos Roofing Addresses This:

We’ve been serving Southwest Florida for 30 years from our Fort Myers location. We’re not going anywhere. When we say we’ll be here for routine inspections, maintenance, and emergency repairs, we mean it. We:

Schedule annual inspections to remove debris and catch early signs of damage

Provide clear documentation for insurance claims when weather causes damage

Offer ongoing maintenance services, including gutter cleaning, moss treatment, and sealant application

Respond promptly when you need us, especially after severe weather events

Stand behind our work with comprehensive workmanship warranties in addition to manufacturer warranties

You can reach us at (239) 267, 6200. We’re a local company with deep roots in Fort Myers, Cape Coral, Naples, Bonita Springs, Estero, Marco Island, and Port Charlotte. Our reputation, including our 2024 Nextdoor Neighborhood FAVES recognition, depends on satisfied customers who trust us year after year.

“How Do I Avoid Costly Surprises Down the Road?”

Your Concern: You want to know the real cost of ownership, not just the installation price. You don’t want hidden maintenance requirements or surprise expenses.

How San Carlos Roofing Addresses This:

After 30 years and hundreds of installations, we believe in education and prevention:

We teach you what to watch for between inspections (water stains, damaged shingles, clogged gutters, granule loss)

We explain maintenance requirements for your specific roof type so there are no surprises that could void your warranty

We help you understand warranty coverage and what regular maintenance is required to keep manufacturer warranties valid

We work with your insurance company to document storm damage and maximize your claim, we know what adjusters need to see

Our goal is educated homeowners who understand their roof and can make informed decisions. That’s why our customers keep referring their friends and neighbors to us.

“Can I Trust Their Reviews and Reputation?”

Your Concern: Anyone can claim they’re the best. You want proof.

How San Carlos Roofing Addresses This:

Don’t just take our word for it, see what your neighbors say:

We’re a 2024 Nextdoor Neighborhood FAVES Winner, recognized by the communities we serve

30 years in business with hundreds of successful installations

Licensed (FL License #CCC1330248) and insured for your protection

We’ve built our reputation one roof at a time over three decades. We protect it by doing quality work and treating every customer with respect and transparency.

The Bottom Line

Choosing a roofing company shouldn’t be a gamble. You need a partner who understands Southwest Florida’s brutal climate, uses quality materials, catches problems early, and stands behind their work for the long haul.

San Carlos Roofing has been that partner for hundreds of Fort Myers area families over the past 30 years. We’re not the cheapest option, we’re the smart option for homeowners who want their roof to last and who value working with a licensed, insured, award, winning local company with a proven track record.

Ready to protect your investment? Call us at (239) 267-6200 or schedule your no, obligation inspection today and experience the difference that three decades of Southwest Florida roofing expertise makes.

Owning a new home is an exciting milestone, and as a homeowner, maintaining your roof is one of the most critical responsibilities. A well-maintained roof not only protects your investment but also ensures the safety and comfort of your home. San Carlos Roofing offers this article provides a comprehensive checklist for roofing maintenance, tailored for new homeowners.

Extends Lifespan: Routine care helps prolong the life of your roof, delaying costly replacements.

Prevents Costly Repairs: Early detection of minor issues can save you from expensive repairs down the line.

Improves Energy Efficiency: A well-maintained roof enhances insulation, reducing energy costs.

Boosts Home Value: A sound, attractive roof enhances curb appeal and market value.

Monthly Checklist

Stay proactive with these monthly tasks:

Inspect for Debris: Clear leaves, branches, and other debris that can trap moisture and cause damage.

Check for Visible Damage: Look for cracks, loose shingles, or other visible signs of wear.

Clear Gutters and Downspouts: Ensure water flows freely to prevent pooling and leaks.

Seasonal Maintenance

Different seasons bring unique challenges. Here’s how to adapt:

Spring/Fall Tasks

Inspect After Storms: Look for damage caused by heavy rain or wind.

Check Attic Ventilation: Proper ventilation prevents moisture buildup, which can lead to mold.

Remove Moss and Algae: These can weaken your roof’s structure if left untreated.

Winter Tasks

Remove Ice Dams and Excess Snow: Prevent leaks by clearing heavy snow and ice dams.

Inspect Insulation: Ensure your attic insulation is adequate to avoid heat loss and ice formation.

Annual Professional Inspection

While DIY maintenance is vital, an annual professional inspection is equally important:

Detect Hidden Issues: Professionals can identify structural weaknesses or other hidden problems.

Ensure Warranty Compliance: Many roofing warranties require regular professional inspections.

Address Overlooked Problems: Trained experts can spot issues you might miss during routine checks.

Tips for New Homeowners

Keep these tips in mind for effective roof care:

Document Maintenance Activities: Keep a log of inspections, repairs, and replacements for future reference.

Invest in Quality Materials: Use durable materials for repairs to ensure longevity.

Schedule Regular Inspections: Consistent evaluations help maintain your roof’s integrity.

Final Thoughts

A well-maintained roof is key to protecting your home and ensuring its longevity. By following this checklist and working with qualified professionals, new homeowners can safeguard their investment and enjoy peace of mind. Start your roofing maintenance journey today and ensure your home remains safe, efficient, and beautiful for years to come. If you live in Southwest Florida and have questions about roof maintenance give the folks at San Carlos Roofing a call.